Nvidia Q1 Earnings Analysis: "Compute Is Revenue. Compute Is Profit."

“AI infrastructure spending is on track to reach $3-4 trillion annually by the end of this decade.”

“Compute is revenue. Compute is profit.”

Jensen Huang, Nvidia CEO.

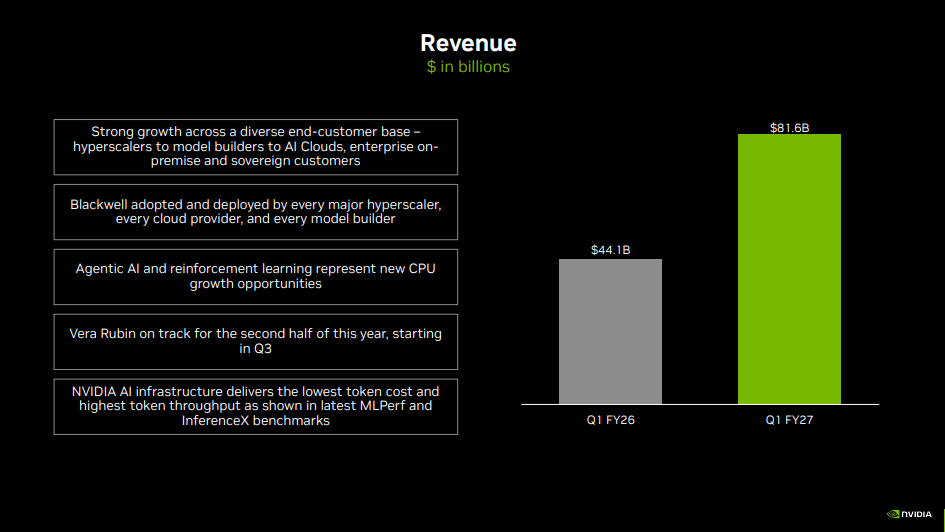

Nvidia ($NVDA) reported its Q1 FY27 results, and the numbers were insane, as usual. The stock also didn’t rally after earnings, as usual, but I’m not looking for one-day gains with this one. Revenue came in at $81.6 billion, up 85% year over year and 20% sequentially. Expectations were $1.77 for EPS and $78.9B for revenue.

Data Center revenue hit $75.2 billion, up 92% from last year. Non-GAAP gross margin was 75%, and the company guided for $91 billion in revenue next quarter (analysts expected $87.3 billion). That guidance also doesn’t assume any Data Center compute revenue from China, which is very important because the outlook is already huge without one of the world’s largest AI markets helping.

On May 6, I told subscribers that I sold half of my SK Hynix position and rotated some of that capital into Nvidia, giving it a Market Outperform (Buy) rating. Since then, Nvidia has moved higher, and I’m reiterating the Buy rating.

The setup made/makes sense. Memory stocks had already run hard, AMD had been strong, CPU-related names were getting attention, and Nvidia had become a relative laggard, even though it still sits at the center of the AI stack.

And after these earnings, I think that setup looks even better. Nvidia didn’t just beat the numbers. It also gave us a clearer picture of why the thesis is more than just selling GPUs to a few giant cloud companies. The company is pushing deeper into AI factories, full systems, networking, CPUs, sovereign AI, enterprise AI, physical AI and edge computing. Basically, Nvidia is trying to become the full infrastructure layer for AI.

Jensen Huang summed up the bull case in the earnings release, saying:

“The buildout of AI factories, the largest infrastructure expansion in human history, is accelerating at extraordinary speed.”

He also said agentic AI has arrived and is already doing productive work.

“Agentic AI has arrived, doing productive work, generating real value and scaling rapidly across companies and industries. NVIDIA is uniquely positioned at the center of this transformation as the only platform that runs in every cloud, powers every frontier and open source model, and scales everywhere AI is produced — from hyperscale data centers to the edge.”

Some quick definitions: An AI factory is basically a data center built to produce intelligence. Instead of just storing data or running normal software, these systems train AI models and serve AI responses. Agentic AI means AI systems that can plan, use tools, write code, search, reason and complete tasks instead of just answering one question. If that takes off, the need for compute keeps rising.

That’s the bull case. Nvidia isn’t selling into a dead-end hardware cycle. It’s selling into a world where AI usage keeps growing, models keep getting more complex, and companies need more infrastructure to make AI useful.

People have been calling for AI spending slowdowns for a while, calling it unsustainable. Maybe it is, but based on this quarter and the ones before it, that slowdown still hasn’t shown up. Quite the opposite, actually.

Let’s get into the results.

Nvidia’s Fiscal Q1-2027 Was Absurd, Growth Is Accelerating

As I said earlier, total revenue was up 85% year over year. Quarter-over-quarter, it was up 20%. In the same quarter last year, growth was 69.2%.

This was Nvidia’s third straight quarter of year-over-year acceleration and its 14th straight quarter of sequential growth. For a company this big, that’s impressive. The company also added $13.5 billion of revenue sequentially, which was a record.

The main driver was still Data Center, and more specifically, Blackwell (Nvidia’s current flagship AI chip platform).

Nvidia’s CFO, Colette Kress, said Nvidia benefited from an inflection in inference demand as it ramped Blackwell systems across hyperscalers, model makers, AI cloud providers and sovereign customers. Inference simply means the part of AI where the model is actually used. Training is building the model. Inference is when the model answers questions, writes code, creates images or does work for users.

Inference demand will keep growing quickly. The more people use AI tools, the more compute is needed to serve those responses. So, when management says Blackwell has the lowest token generation cost in inference, that means customers can run AI more efficiently and potentially more profitably. Tokens are basically the small pieces of text, code or other data that AI models process and produce.

Networking is becoming part of the moat

Nvidia recently changed how it reports its business (more on that later), but it still gave investors the old breakdown for comparison. On that basis, Data Center compute revenue was $60.4 billion, up 77% year over year. Data Center networking revenue was $14.8 billion, up 199% year over year and 35% quarter over quarter.

The networking number is especially important because it shows Nvidia’s moat isn’t just the GPU anymore. These AI data centers need GPUs, but they also need extremely fast networking to connect everything together. If the chips can’t communicate quickly, the whole system becomes less efficient (side note: Broadcom is also a networking player. See my Broadcom deep dive here).

That’s why I think the “Nvidia is just a GPU company” argument is getting weaker. Yes, GPUs are still the core of the story. But the company is increasingly selling full systems, including GPUs, networking, CPUs, software, racks and the ecosystem needed to make massive AI data centers work.

Margins Are Still Ridiculous

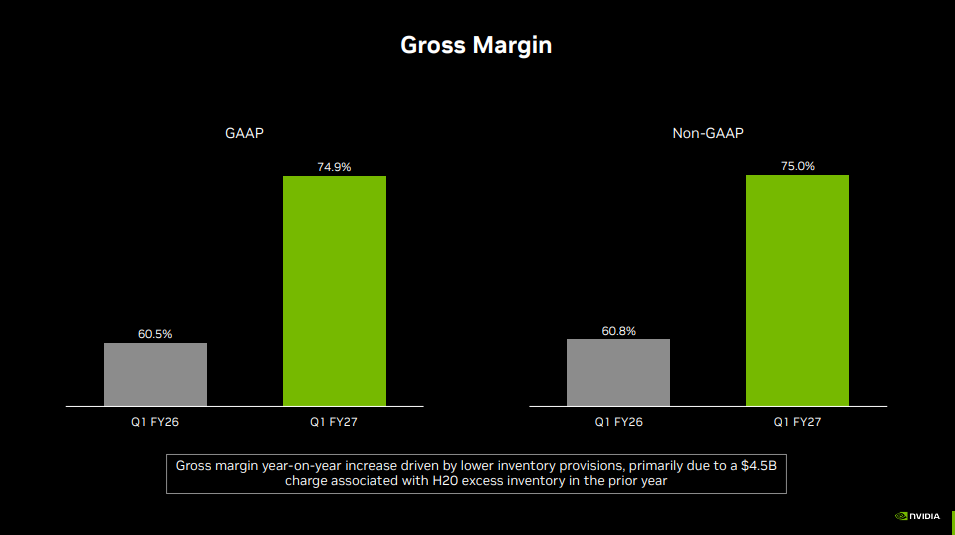

Nvidia reported GAAP gross margin of 74.9% and non-GAAP gross margin of 75%. That’s ridiculous for a company selling physical hardware.

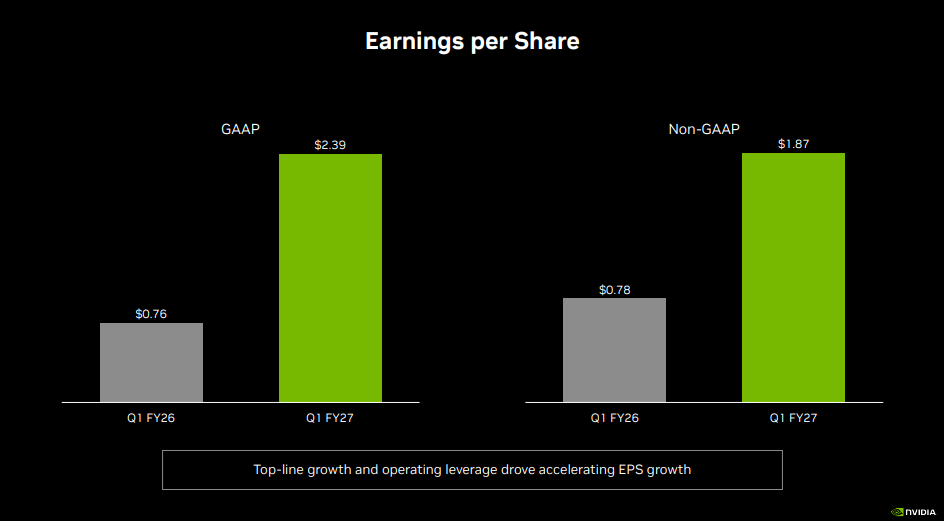

GAAP operating income was $53.54 billion, up 147% year over year. Non-GAAP operating income was $53.78 billion, also up 147%. Non-GAAP EPS was $1.87, up 140% from last year.

The GAAP net income number needs context

One thing to note, though, is that GAAP net income included a big gain from equity securities. So I think non-GAAP net income of $45.5 billion is probably the cleaner number to look at for the actual operating business. Either way, the profitability was strong.

Free Cash Flow Is Flowing Back To Shareholders

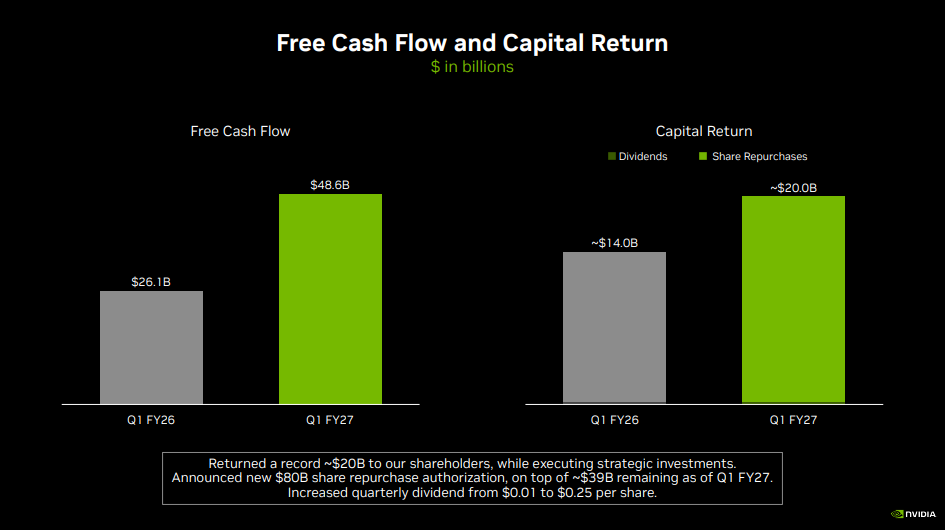

Nvidia also returned about $20 billion to shareholders in Q1 through buybacks and dividends. The company announced a new $80 billion share repurchase authorization, on top of around $39 billion remaining as of Q1. It also increased the quarterly dividend from $0.01 to $0.25 per share. Finally, a dividend that isn’t a complete joke.

Free cash flow was $48.6 billion in Q1, up from $26.1 billion last year. That’s a massive number. And when a company has that much cash coming in, it has options. It can secure supply. It can invest in the ecosystem. It can buy back stock. It can raise the dividend. It can do all of those things at the same time.

Enjoying this article so far? Please consider subscribing to my Substack to support my work!

Edge Computing And Physical AI Are On The Come-Up

Data Center is still the main story. But Nvidia’s Edge Computing segment is worth watching too. Edge Computing revenue was $6.4 billion, up 10% sequentially and 29% year over year.

In simple terms, edge computing means AI running closer to where the work actually happens, instead of only inside giant cloud data centers. That includes PCs, workstations, cars, robots, factories, telecom equipment and other devices or systems outside the traditional cloud.

That’s where physical AI comes in. Physical AI basically means AI that interacts with the real world. Think robots, autonomous vehicles, industrial machines, medical instruments and telecom systems. It’s not just a chatbot sitting on a screen. It’s AI controlling or helping physical systems.

Colette said physical AI revenue exceeded $9 billion over the last 12 months. Nvidia also highlighted autonomous driving, robotics, AI-RAN, industrial software and other edge opportunities in its results.

Side note: Ouster ($OUST) is a pretty interesting physical AI company that I recently talked about, if you want to check that article out below.

Ouster (OUST) Jumped 26%. Is This The Next Physical AI Trade?

Nvidia’s New Segment Structure

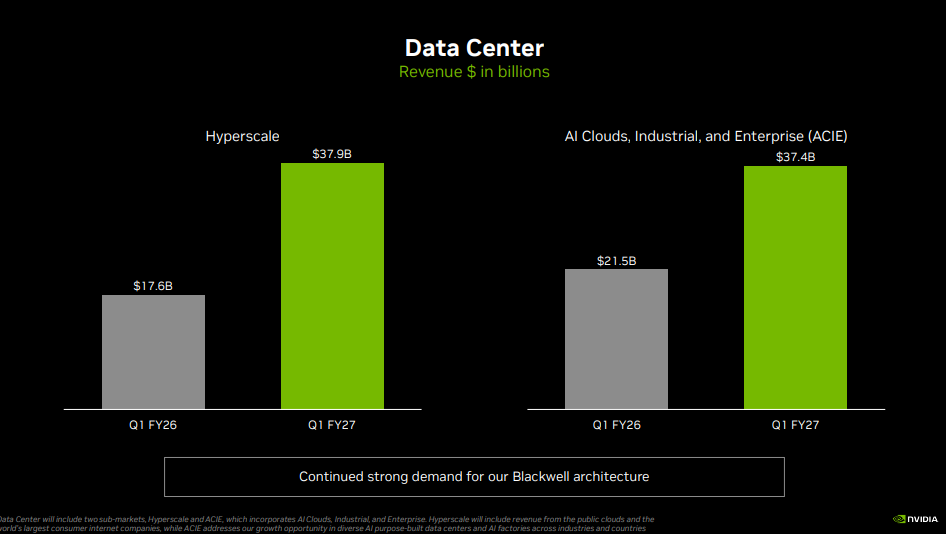

Hyperscale is still huge, but ACIE is something to watch

Going forward, NVDA will have two main platforms for reporting purposes: Data Center and Edge Computing.

From the press release:

Within Data Center, NVIDIA will report two sub-markets, Hyperscale and ACIE, which incorporates AI Clouds, Industrial and Enterprise. Hyperscale will include revenue from the public clouds and the world’s largest consumer internet companies, while ACIE addresses NVIDIA’s growth opportunity in diverse AI purpose-built data centers and AI factories across industries and countries. Edge Computing highlights data processing devices for agentic and physical AI including PCs, game consoles, workstations, AI-RAN base stations, robotics and automotive.

This helps answer one of the biggest questions around Nvidia. Is this business just five or six mega-cap tech companies buying GPUs? Or is the customer base getting broader?

Based on the quarter, the answer seems to be both. The hyperscalers are still spending a ton of money. But Nvidia is also showing that AI clouds, industrial companies, enterprises and sovereign customers are big revenue drivers as well. The investor presentation showed Hyperscale revenue rising from $17.6 billion in Q1 FY26 to $37.9 billion in Q1 FY27, while ACIE revenue rose from $21.5 billion to $37.4 billion.

The Guidance Was Impressive

Nvidia guided to $91 billion in revenue

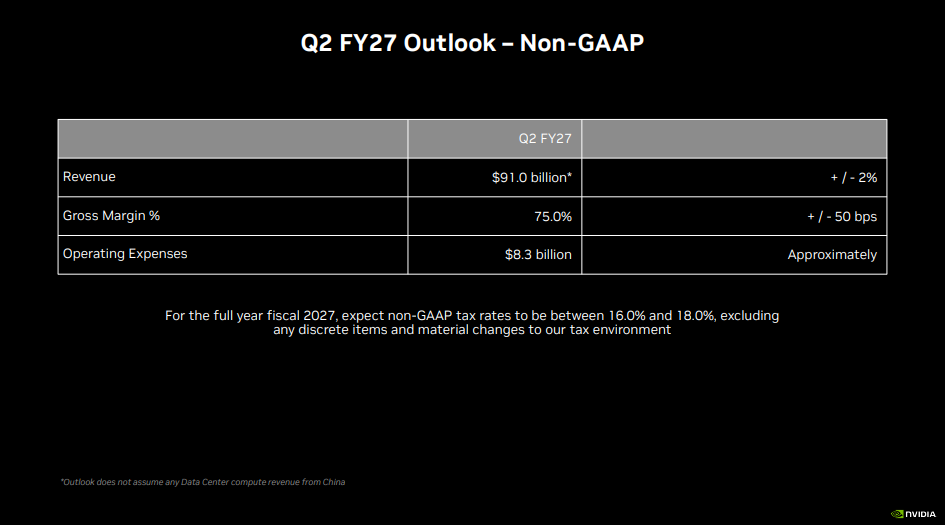

Nvidia guided for $91 billion in revenue, plus or minus 2%. That’s up from $81.6 billion in Q1. The company also guided for non-GAAP gross margin of 75%, plus or minus 50 basis points, and non-GAAP operating expenses of about $8.3 billion. The $91B guidance for next quarter also suggests a 100% YoY growth rate to come. More acceleration.

And here’s the thing: Nvidia isn’t assuming any Data Center compute revenue from China in its outlook. That’s the same point I highlighted back in February. The guide is strong without China. So, if China stays restricted, Nvidia is still growing at an absurd pace. If China eventually comes back in a meaningful way, that could be a little bit of icing on the cake.

Nvidia’s CPU Business Is Real

This was one of the biggest parts of my thesis

The most interesting part of the call for me was the CPU discussion. This was part of my thesis going into earnings. Nvidia is still treated by many investors as a GPU company, but its systems increasingly include CPUs too.

Management said during the earnings call:

“We have visibility to nearly $20 billion in total CPU revenue this year, setting us up to become the world leading CPU supplier.”

And that’s standalone CPU revenue, according to Jensen, not GPUs that come with some CPUs attached.

If the market starts to understand that Nvidia is also becoming a serious CPU player, that could help the stock.

Nvidia also said Vera CPU opens a new $200 billion total addressable market for the company.

Why CPUs matter for agentic AI

The reason CPUs matter for agentic AI is pretty simple. The GPU does the heavy AI math. The CPU helps manage the workflow around it. If an AI agent is browsing the web, using tools, managing memory, compiling code or coordinating tasks, a lot of that work needs CPUs.

So, the CPU opportunity doesn’t necessarily replace the GPU opportunity. It can expand the total system Nvidia sells.

Blackwell Is Still the Engine

The demand still looks extremely strong

Blackwell was everywhere in this report. The investor presentation said Blackwell has been adopted and deployed by every major hyperscaler, every cloud provider and every model builder.

Colette Kress also said demand for GB300 and NVL72 was particularly strong. In simple terms, these are Nvidia’s latest Blackwell AI systems, with NVL72 connecting dozens of Blackwell GPUs together inside one rack. Frontier model builders and hyperscalers have already cumulatively deployed hundreds of thousands of Blackwell GPUs, which Colette called the fastest product ramp in Nvidia’s history.

The key thing is that Nvidia isn’t only saying Blackwell is fast. It’s saying Blackwell gives customers the lowest token generation cost in inference. That’s the important part. If customers can generate tokens more cheaply, then AI applications become easier to scale. And if AI applications become easier to scale, Nvidia keeps benefiting from the usage growth.

Vera Rubin is next

Vera Rubin is the next product cycle. The investor presentation says Vera Rubin is on track for the second half of this year, starting in Q3.

One analyst asked how investors should think about the Vera Rubin ramp compared to GB300. Colette didn’t promise it would be faster, but she said Nvidia has demand planned, purchase orders in place and almost all major customers ready to go. That’s enough for me. It suggests that demand visibility is strong beyond the current quarter.

AI Infrastructure Spending Could Still Get Much Bigger

Management said AI infrastructure spending is on track to reach $3 trillion to $4 trillion annually by the end of this decade. That number sounds insane, but it explains why Nvidia keeps talking about AI factories instead of just chips. If AI usage keeps growing, companies need more GPUs, CPUs, networking, power, cooling, racks and software to support it.

Jensen summed it up in three lines:

“Demand has gone parabolic.”

“Tokens are now profitable.”

“Compute is revenue. Compute is profits.”

That’s the thesis. Nvidia is saying customers can now make money from AI usage. If they can make money from AI usage, they need more compute. And if they need more compute, Nvidia benefits.

This is the key question is: are hyperscalers overspending on AI? Or are they building infrastructure that will generate real revenue? Nvidia is clearly arguing the second one.

And for now, the numbers back that up. If AI demand were fake or already slowing, Nvidia would not be guiding to $91 billion in quarterly revenue while keeping gross margins around 75%.

The risk is that the $3 trillion to $4 trillion infrastructure vision ends up being too optimistic. If AI apps don’t generate enough revenue, or if customers realize they overbuilt capacity, Nvidia would feel that quickly.

The Bottom Line On Nvidia Stock

The bottom line is that Nvidia is still alive, more alive than ever, even if the stock has been a laggard. The company crushed the quarter, guided to $91 billion in revenue, held 75% non-GAAP gross margins, and showed that demand for Blackwell, networking, CPUs and full AI systems is still extremely strong. The China issue also isn’t carrying the outlook, which makes the guidance even cleaner.

The stock isn’t risk-free, especially if AI capex eventually slows or the $3 trillion to $4 trillion infrastructure vision proves too optimistic. But right now, the numbers are still moving in Nvidia’s favor. I’m still long Nvidia and still rate the stock a Buy because the quarter made the thesis look stronger, not weaker.

Disclaimer: This is NOT professional advice. Please do your own due diligence before making any decisions.

If you like this article, please consider subscribing. Paid subs get full access to past and future deep dives, as well as weekly watchlists with actionable ideas. 7-day free trials are available as well!