Ouster (OUST) Jumped 26%. Is This The Next Physical AI Trade?

A fresh NVIDIA DRIVE catalyst, a clean breakout above $30, and real Q1 growth make Ouster more than just another lidar spike.

Rating: Market Outperform (Speculative Buy)

Market cap: $2.18B

Ouster ($OUST) jumped 26% after the market finally got the kind of setup it loves in this environment: a fresh NVIDIA-related catalyst, a clean Physical AI story, and a major breakout above the ~$30 level on heavy volume. The move was definitely helped by hype on X, but I don’t think this was just another random lidar spike.

Ouster now has a real catalyst, a stronger product cycle, accelerating revenue growth, and a stock chart that suddenly looks much more interesting.

Anyway, the key news came out yesterday: Ouster said its Rev8 OS digital lidar sensors are now compatible with NVIDIA DRIVE Hyperion, a platform used to help develop level 4 autonomous vehicles. After that headline hit, traders had more of a reason to care.

Ouster now has Rev8 tied to NVIDIA DRIVE Hyperion for autonomous vehicles, Rev8 integration across NVIDIA Jetson for robotics and edge AI, and a stronger Physical AI story after buying Stereolabs. In a speculative market where AI-adjacent names are working, that kind of setup can move fast.

Physical AI basically means AI moving from software into the real world. Instead of just chatbots or cloud software, think robots, self-driving vehicles, smart intersections, drones, industrial machines, warehouses, and equipment that needs to understand what’s around it before it can act. That’s where Ouster fits in.

The company makes lidar sensors, cameras, AI compute, and perception software. Lidar uses laser pulses to create a 3D map of the world, helping machines understand distance, shape, movement, and surroundings.

Ouster just reported strong Q1 growth, launched Rev8, expanded beyond lidar through Stereolabs, and now has two different NVIDIA-related angles investors can understand.

The numbers make the story more interesting. In Q1 2026, Ouster generated about $49 million of revenue, up 49% year over year. It shipped more than 12,600 sensors, including over 8,300 lidar sensors and over 4,300 camera sensors. GAAP gross margin was 43%, non-GAAP gross margin was 46%, and the company ended the quarter with $175 million in cash, cash equivalents, restricted cash, and short-term investments, with no debt.

Management also said this was Ouster’s 13th straight quarter of product revenue growth. Royalty revenue also wasn’t material in Q1, so the growth mostly came from selling actual products, not from a one-time licensing boost. That makes the quarter cleaner than it would be if the growth had been padded by unusual royalty revenue.

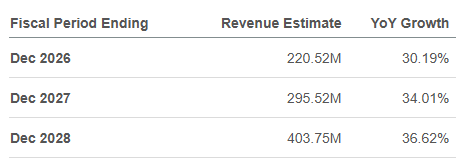

So the setup is pretty clear. Ouster isn’t a fake AI stock with no real business behind it. But it also isn’t cheap anymore. At a $34.17 share price and a $2.18 billion market cap, Ouster trades at about 10x 2026 consensus revenue estimate of $220.5 million. That multiple falls to about 7.4x 2027 revenue, and 5.4x 2028 revenue, if the company hits the estimates shown below.

Put simply, investors are already paying for a lot of future growth. The stock can still work if revenue keeps climbing quickly, but after this move, there isn’t much room for disappointment. If Rev8 adoption is slower than expected, if growth cools, or if profitability gets pushed further out, the valuation can become a problem fast.

That’s why I’d rate Ouster a Speculative Market Outperform (Buy rating), not a traditional medium or long-term Buy rating.

I think the stock can keep working in this market because the catalyst, chart, volume, and Physical AI story are all lined up. But this is still an unprofitable and cash-flow negative company, so I wouldn’t treat it like a proven long-term compounder yet.

I can change my mind quickly on this one if things start drying up.

Source: Finbox

Treating Ouster As A Trade First

Ouster may become a much better business over time, but right now, the stock is mostly a momentum setup. The NVIDIA DRIVE Hyperion headline gave traders a catalyst. The reaction to that news helped the stock break above $30. The attention on X brought more eyes to the name. And the fundamentals are good enough to make the story feel real instead of completely empty.

That’s the kind of setup that can keep running, especially in this market cycle.

People need to stop underestimating market cycles. Sometimes, certain types of stocks work better than others.

Speculation is working right now.

Smaller AI-related names, robotics plays, infrastructure-adjacent companies, and high-growth tech stocks can move quickly when the chart, volume, and story line up.

Sometimes the market rewards patience and valuation discipline. Other times, it rewards speed, momentum, and being early to a story that other traders are just starting to notice.

Ouster fits the second bucket right now.

For me, the fundamentals are not enough to make this a long-term core holding yet.

If you’re an OUST bull reading this, don’t shoot me please.

The company still has to prove that Rev8 adoption can turn into sustained revenue growth and real profitability.

Instead, the fundamentals are more useful for judging how much fuel the momentum story has.

If estimates start moving higher because Rev8 demand is stronger than expected, the story gets more fuel. If volume stays strong and the stock keeps holding the breakout, the trade can keep working. But I wouldn’t stubbornly hold a large position in an unprofitable company just because the long-term story sounds exciting.

I’ve been in the market for a long time, and I’ve heard many “exciting” stories that don’t play out.

3D printing, EVs, SPACs, weed stocks. You name it.

That’s why the prior breakout area is important. If the stock loses the high-$20s, near where it was before the breakout, the setup gets weaker. A stop-loss around that area (under $28 ish for now) can make sense for someone treating this as a momentum trade instead of a long-term investment.

Looking further out, the chart is interesting because it’s been consolidating for some time now and can make another swing high if momentum stays. The next target would be $50 if it breaks the most recent swing high of about $42.

Let’s Look More Into The Catalysts

The direct catalyst was the NVIDIA DRIVE Hyperion news. Ouster said its Rev8 OS sensors are qualified to run on NVIDIA DRIVE Hyperion, which is designed to help developers build and deploy level 4 autonomous vehicles.

Level 4 autonomy means a vehicle can drive itself in certain areas or conditions without needing a human to take over. It doesn’t mean every car can drive itself everywhere, but it’s still an advanced form of autonomy. Robotaxis, autonomous trucks, and self-driving shuttles are the types of markets investors usually think about when they hear level 4 autonomy.

That’s why investors reacted to the headline. Rev8 is now tied more directly to autonomous driving and robotaxi development. That gives the market a simple way to understand the story: if autonomous vehicles need better sensors, and Ouster’s sensors can work inside NVIDIA’s autonomous-driving development platform, Ouster could have a more relevant role in that ecosystem.

The key point is that Ouster isn’t just saying Rev8 is a better sensor by itself. The company says its sensors have optimized plugins for NVIDIA DriveWorks SDK. In plain English, that means developers can feed Ouster’s 3D sensor data directly into NVIDIA’s software tools more easily. Developers don’t just want good hardware. They want hardware that fits into the systems they’re already building with.

But this doesn’t mean NVIDIA has picked Ouster as the winner. It doesn’t guarantee huge revenue. What it does is make the autonomous vehicle angle more credible. Ouster is positioning Rev8 inside a development ecosystem used for level 4 autonomy, and the market clearly liked that.

Why The NVIDIA Story Goes Beyond Autonomous Driving

The DRIVE Hyperion news was the more obvious reason for the recent move, but it isn’t the only NVIDIA-related angle. Ouster also announced Rev8 integration across NVIDIA Jetson, with support across NVIDIA JetPack, Isaac Sim, Jetson AGX Orin, and Thor.

Basically, NVIDIA Jetson is a family of computing platforms used in robots, drones, cameras, industrial machines, and other edge AI systems. Edge AI means the AI processing happens close to the machine itself instead of sending everything to a cloud data center. For example, a warehouse robot needs to react quickly. It can’t always wait for data to travel back and forth from the cloud.

So Jetson supports the robotics and edge AI side of the story. DRIVE Hyperion supports the autonomous vehicle side. Together, they give Ouster two different NVIDIA-related narratives. One is about robots and machines. The other is about autonomous vehicles.

This shouldn’t be overhyped. Ouster being compatible with NVIDIA platforms doesn’t just turn it into a massive winner. But it can reduce friction for developers and customers. It also gives investors a cleaner way to understand the company. Ouster isn’t just selling lidar sensors. It’s trying to become part of the perception stack for machines that need to sense and act in the real world.

What Rev8 Actually Does

Rev8 is the center of the story. Ouster calls it the world’s first native color lidar. That basically means the sensor combines 3D lidar data and color directly on silicon.

Normal lidar can tell a machine the shape and distance of objects around it. Rev8 is trying to add more visual context to that 3D data. That means it’s not just helping a machine know that something is in front of it. It can help the machine better understand what it’s looking at.

That could be useful because machines don’t just need to detect objects. They need context. They need to understand signs, brake lights, road surfaces, object boundaries, textures, distance, movement, and depth. A self-driving system doesn’t just need to know a car is nearby. It may also need to understand whether brake lights are on, where the lane markings are, or how far away a small object is.

That’s why native color lidar could be useful. It’s not just about prettier point clouds. A point cloud is basically a 3D map made up of millions of data points. If those data points include better color and depth information, machines may get richer data to train on and operate with.

The specs are strong enough to support the excitement. The flagship OS1 Max offers 256 channels of high-definition sensing, up to 500 meters of range, and a 45-degree vertical field of view. In simple terms, that means it can capture a lot of detail, see far, and cover a wider vertical area. Rev8 is also auto-grade, cybersecure, and designed for functional safety certifications like ASIL-B, SIL-2, and PLd.

Those safety certifications are important because Ouster is trying to sell into serious industrial and automotive markets. If a sensor is going to help a vehicle, robot, or machine make decisions in the real world, customers need reliability and safety standards. It can’t just be a cool demo product.

Ouster also says Rev8 was designed to be more affordable and more scalable than Rev7, with a planned 10-year production life. That’s a big part of the bull case. A breakthrough sensor isn’t enough if it’s too expensive, too hard to deploy, or too difficult to integrate. Ouster needs Rev8 to scale into real commercial programs.

Management also said dozens of companies across industrial, robotics, automotive, and smart infrastructure markets intend to adopt Rev8 OS sensors. The list included names like Google, Volvo Autonomous Solutions, Liebherr, Epiroc, Field AI, Skydio, PlusAI, Bedrock, Seegrid, Gecko Robotics, Cyngn, and others.

That doesn’t guarantee revenue from all of them. “Intend to adopt” is not the same as “signed massive contract.” But it does show Rev8 isn’t launching into silence. There’s already customer interest across multiple end markets.

Why Ouster Is No Longer Just A Lidar Company

The Stereolabs acquisition is another reason the story has changed. Ouster acquired Stereolabs in February, adding AI camera vision, stereo cameras, edge compute, and perception software. In Q1, Stereolabs contributed about seven weeks of revenue and helped push camera shipments above 4,300 units.

This doesn’t transform the company overnight, but it changes what Ouster is trying to become. The company isn’t trying to be just a lidar supplier anymore. It’s trying to offer a fuller perception stack that includes lidar, cameras, AI compute, sensor fusion, perception software, and AI models.

A perception stack just means the full set of tools a machine uses to understand the world around it. Lidar can provide depth and structure. Cameras can provide visual information. Compute can process the data. Software can turn that data into decisions or useful insights.

That’s a better story because pure hardware businesses can be fragile. If you only sell one type of sensor, customers may switch suppliers, competitors may copy features, and pricing can come under pressure. A broader platform can become more valuable if it reduces integration headaches and gives customers better unified data.

This is where the Physical AI thesis makes sense. Machines need multiple ways to understand the real world. Ouster is trying to combine those pieces instead of selling one piece in isolation.

That’s much more interesting than standalone lidar.

Where Ouster Is Already Seeing Demand

The commercial side is stronger than the typical lidar hype story. Ouster said its lidar business grew about 44% year over year, helped by industrial demand. The company pointed to several large industrial automation deals, including an expanded long-term relationship with a European industrial company for port automation and a deal with an autonomous earthmoving company tied to a U.S. Department of Defense project.

This shows Ouster isn’t only relying on future robotaxi dreams. Industrial automation is already happening. Port automation is already happening. Heavy equipment autonomy is already happening. These are markets where better sensing can solve real problems today.

For example, a port can use sensors to help automate the movement of containers and equipment. A construction or mining machine can use sensors to understand its surroundings. A smart traffic system can use sensors to detect vehicles, pedestrians, and traffic flow. These are practical uses, not just futuristic investor-deck ideas.

Smart infrastructure also deserves attention. Ouster BlueCity now has more than 700 contracted site deployments across intersections, mid-blocks, and highways. The company also expanded BlueCity with the Georgia Department of Transportation for more than 30 intersections across the Greater Atlanta area ahead of the FIFA World Cup. Ouster Gemini is operating at more than 550 sites globally.

BlueCity is Ouster’s traffic management solution. In simple terms, it helps cities use lidar and software to monitor and manage traffic more intelligently. Ouster Gemini is used for security, monitoring, and awareness across physical sites. These aren’t as exciting as robotaxis, but they may be more grounded.

Cities and transportation departments move slowly, but once they adopt a system and expand it, the revenue can become stickier than investors expect. That gives Ouster a practical base of demand instead of relying only on futuristic markets.

That’s one of the biggest reasons I don’t think the move is pure hype. Ouster has current revenue, current deployments, current customers, and real end markets. The future still has to be proven, but the company isn’t starting from zero.

The Valuation Already Prices In A Lot Of Growth

The valuation is the main pushback. At $34.17 per share and a $2.18 billion market cap, Ouster trades at about 10x 2026 revenue. That’s not crazy for a fast-growing AI and robotics-adjacent company, but it’s not cheap either.

However, the stock doesn’t need to look cheap on current numbers if the company grows fast enough.

But that’s also the risk. Investors aren’t paying for Ouster as it exists today. They’re paying for Rev8 adoption, Stereolabs integration, continued smart infrastructure growth, industrial demand, NVIDIA ecosystem relevance, and a path to profitability. If any of those pieces disappoint, the multiple can contract quickly.

Earnings don’t help much yet either. Consensus expects Ouster to lose about $0.30 per share in 2026 and earn only around $0.03 per share in 2027. That means this is still a revenue growth and operating leverage story.

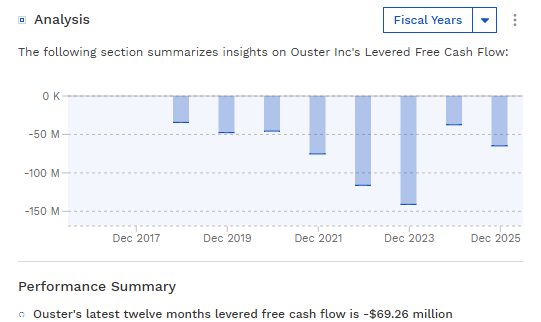

Ouster is also still cash-flow negative. Based on the data shown, its latest twelve-month free cash flow was about negative $69 million. The good news is that the company had $175 million of cash as of Q1 and no debt, so it has room to execute. It also launched a $100M ATM offering just a few days ago. It has a few years of runway at the current cash burn rate, but this is still not a self-funding compounder yet.

Management’s long-term framework is 30% to 50% annual revenue growth, 35% to 40% GAAP gross margin, and controlled operating expense growth. The company is also working toward positive operating free cash flow and profitability.

That gives investors a framework. But Ouster still has to prove it.

What Could Make The Bull Case Work

To recap:

The bull case is that Ouster is moving from “lidar company” to “Physical AI perception platform.”

That’s a much better category. If machines are going to operate more intelligently in the physical world, they need better perception. Ouster now has lidar, cameras, AI compute, perception software, sensor fusion, smart infrastructure solutions, and NVIDIA ecosystem compatibility. That gives the company a much more complete story than it had before.

Rev8 is the product catalyst. Stereolabs broadens the platform. BlueCity and Gemini give the company real infrastructure traction. Industrial automation gives it practical enterprise demand. Jetson strengthens the robotics angle. DRIVE Hyperion strengthens the autonomous vehicle angle. The Q1 numbers show the company is already growing. The breakout shows the market finally cares.

That’s why the stock can keep working.

What Could Go Wrong

The risk is that investors start treating a momentum trade like a guaranteed long-term investment.

Ouster doesn’t have a fortress moat (a durable competitive advantage that protects a company from competitors). Think network effects, high switching costs, patents that are hard to get around, or a brand that customers trust so much they won’t leave. Ouster has differentiated technology, a better product cycle, growing commercial traction, and a broader platform after Stereolabs. That’s good, but it’s not the same as being untouchable like a Visa or Mastercard.

Customers still have alternatives. Competitors still exist. Pricing still counts. Product launches still need to convert into volume. And the company still needs to prove that revenue growth can turn into durable profitability.

The lidar industry has also burned investors before. There have been too many huge TAM (total addressable market) stories, too many investor decks, and not enough profitable businesses. A big TAM sounds exciting, but it doesn’t automatically mean one company will capture it profitably.

Ouster looks better positioned than many of those old lidar names, but investors shouldn’t ignore the industry’s history.

The NVIDIA headlines are another risk if people overread them. Remember, Jetson integration and DRIVE Hyperion qualification don’t automatically mean massive revenue is coming. They improve Ouster’s ecosystem positioning. They don’t replace the need for actual customer adoption and financial execution.

The Takeaway On OUST Stock

I don’t think Ouster is just another lidar pump. The stock moved because the market had a real catalyst to grab onto: NVIDIA DRIVE Hyperion compatibility, Rev8 momentum, a cleaner Physical AI story, strong Q1 growth, and a breakout above a key technical level. X hype helped amplify the move, but the story wasn’t empty.

That said, I’m treating this as a Speculative Market Outperform (Buy) rating, not a traditional long-term Buy. Ouster is still unprofitable, cash-flow negative, and trading around 10x 2026 revenue, so the stock needs continued execution. If the chart, volume, catalyst, and story keep working together, the trade can keep working. If momentum dries up, I’d treat it very differently.

Disclosure: I have a small position in OUST stock from around $31.50, and this is just my personal opinion. This is NOT professional advice. Please do your own due diligence before making any decisions.

If you like this article, please consider subscribing to my Substack, where you can find the original article here.

Paid subs get full access to past and future deep dives, as well as weekly watchlists with actionable ideas. 7-day free trials are available as well!