SpaceX Deep Dive ($SPCX): Is the Biggest IPO in History Worth Buying?

SpaceX ($SPCX) goes public this Friday, June 12th. $75 billion raise. $1.75+ trillion valuation. Biggest IPO in history. Most retail investors have been waiting years for this moment.

And honestly, I get the excitement. SpaceX is one of the most important companies in the world. It dominates launch, Starlink is becoming a monster business, and the long-term AI opportunity could be enormous if the company actually pulls it off.

But at $135 per share, I don’t think this is an easy long-term buy. The IPO price already assumes a lot goes right across rockets, Starlink, and xAI, while the AI segment is still losing billions and absorbing most of the company’s capital spending. So for me, this is more interesting as a potential day-one momentum trade than a stock I want to blindly hold for the next decade.

But before you do anything, you need to actually understand what you’re buying. Let’s break it all down.

What Does SpaceX Do?

Most people hear SpaceX and think rockets. But that’s only one piece of the puzzle. SpaceX today is really three different businesses operating under one roof, and they’re at very different stages of maturity. The prospectus breaks them out as Space, Connectivity, and AI.

Simplified: the rockets get things into space, Starlink beams internet down from space, and xAI/Colossus is the AI and data center arm that Musk merged into SpaceX earlier this year. Each business has a completely different risk profile, different economics, and a different timeline to profitability.

Business #1: The Rocket Business (Space Launch)

This is where SpaceX started. SpaceX launches satellites, cargo, astronauts, and commercial payloads into orbit. The reason this business is special is reusable rockets.

Before SpaceX, rockets were essentially thrown away after one use. That made launches incredibly expensive and limited who could afford to go to space. SpaceX cracked the code on landing rockets and flying them again, which collapsed the cost per kilogram to orbit and made every competitor look prehistoric by comparison.

The result is that SpaceX now controls roughly 80% of global mass put into orbit. Blue Origin is years behind. ULA is expensive. There is no credible near-term challenger at the scale SpaceX operates at.

The unit economics here are the best of the three segments, with gross margins running around 67% in 2025. The catch is growth has been slow recently, up only about 7.6% year over year in 2025. It’s the backbone of the company, but it’s not the growth engine right now. It’s also what enables the other two businesses, since you need rockets to put up Starlink satellites and to eventually build out AI infrastructure in orbit.

Business #2: Starlink (Connectivity)

If you’re buying SpaceX for one reason, this is it.

Starlink is a satellite broadband network. Instead of relying on fiber cables or cell towers that don’t reach remote areas, Starlink beams internet from a constellation of satellites in low Earth orbit. It serves customers on ships, planes, in rural areas, disaster zones, and anywhere else terrestrial internet can’t reach. Per satellitemap.space, “There are currently 10600 active Starlink satellites in orbit out of a planned constellation of 42,000.”

Starlink had $11.4 billion in revenue in 2025, up nearly 50% year over year. Subscriber count hit 10.3 million in Q1 2026, up from about 5 million a year earlier. Gross margins improved from 37% in 2024 to 48% in 2025. It’s the only segment in the entire company running a positive operating income.

Starlink is what funds everything else. It funds the rocket R&D. It funds the AI buildout. Without Starlink, the whole financial picture looks a lot worse.

The one warning sign is average revenue per user. It dropped from about $99 per month in 2024 to $86 per month in Q1 2025 to $66 per month in Q1 2026. SpaceX has been deliberately moving downmarket with cheaper plans to attract more users, which explains part of the decline. But if subscriber growth ever stalls, that pricing compression becomes a real problem fast.

Amazon Leo is the most credible competitor, but with roughly 330 satellites deployed versus Starlink’s 10,000+, it’s still well behind. To compete in this business, you need to build and launch thousands of satellites before you have a useful network, which creates a massive barrier to entry. SpaceX’s head start is enormous and hard to replicate quickly.

Business #3: The AI Segment (xAI, Colossus, Grok, X)

This is where things get more complicated.

Earlier this year, SpaceX merged with xAI, Elon Musk’s AI company. The combined entity now includes Grok (the chatbot), the Colossus data centers in Memphis (currently among the largest AI compute clusters in the world), and X/Twitter.

The AI segment generated about $3.2 billion in revenue in 2025 but lost about $5.9 billion at the operating level. The gross margins were the worst of the three segments and they deteriorated from 2024 to 2025, not improved. That’s not a good trend in a segment that’s also absorbing the majority of the company’s capital spending.

However, SpaceX recently announced two very large AI infrastructure contracts that change the near-term revenue picture quite a bit.

The Anthropic deal: $1.25 billion per month through May 2029. Anthropic is paying SpaceX to use the Colossus compute capacity.

The Google deal: roughly $920 million per month from October 2026 through June 2029.

Combined, that’s close to $2 billion per month in contracted AI infrastructure revenue.

Here’s the catch, though.

Both contracts have termination clauses. Google and SpaceX can each walk away after December 31, 2026 with 90 days notice. So the “locked in through 2029” narrative ain’t exactly it. These are more like rolling contracts with an opt-out window.

The deeper issue with the AI segment is what Steve Eisman said in his CNBC interview on June 8th. In case you don’t know, Eisman is the Big Short investor who bet against subprime mortgages. He’s not shorting SpaceX, but he’s not buying it either. His exact words: “Despite the incredible sums of money that are being spent, what’s being produced in terms of LLMs and agentic AI is not really differentiable. It’s very commoditized. People are switching constantly from one to the other. There are no moats.”

He has a point. Grok isn’t winning the AI model race right now, and the AI segment looks more like a bet on compute infrastructure than a proven standalone product. That’s meaningful upside if SpaceX can monetize demand, but it’s not the kind of durable AI moat the prospectus wants investors to imagine.

Does SpaceX Have a Moat?

The word “moat” (or competitive advantage) gets thrown around too loosely. Does SpaceX have one? In some places, yes, in some, no.

The Space business: Yes, it has a moat.

SpaceX completed 165 orbital launches in 2025, accounting for almost 51% of all global launches and 85% of all satellites launched that year. In Q4 2025 alone, it held 97% of the U.S. launch market and 83% globally. The reusable rocket economics create a cost per kilogram to orbit that no competitor can match. Blue Origin has been trying for over a decade and is still years behind on orbital capability. ULA still charges enough more than SpaceX to keep Falcon 9 looking like the value option.

The moat also has a flywheel: the more SpaceX launches, the more data they collect, the better the rockets get, the cheaper launches become, the harder it is for competitors to close the gap.

One investor told Fortune: “It’s a truly unique business with the deepest moat that exists today. This company launches over 90% of Western payload into space each year. It’s like if you own the only undersea cable from the U.S. to Europe.” Fortune, May 2026

Starlink Business: Yes, there’s a moat, but watch the pricing.

Morningstar themselves confirmed that Starlink has an economic moat, noting that two-thirds of SpaceX’s 516 launch payloads since 2019 were dedicated to Starlink, which means the launch and connectivity businesses are self-reinforcing. To compete, you need to build and launch thousands of satellites before you have a network worth subscribing to.

The concern, though, is pricing. As I mentioned earlier, the average revenue per user dropped from about $99 per month in 2024 to $66 per month in Q1 2026.

AI Business: No moat yet.

Morningstar calls xAI’s moat “indeterminate” and describes the AI segment as “a material threat of value destruction” for the overall company. Colossus exists, the contracts are signed, but renting compute to Google and Anthropic isn’t the same as owning a product people can’t live without. And the companies paying SpaceX for that capacity are also building their own.

The orbital data center thesis is an interesting long-term AI story in the prospectus. But SpaceX doesn’t expect to even begin deploying orbital AI compute satellites until 2028 at the earliest, and the technology is still completely unproven at commercial scale.

TL;DR

The IPO price values SpaceX like all three segments have deep permanent moats. Launch does. Starlink mostly does. AI doesn’t yet. You’re paying for a moat that’s only partially built, and the segment absorbing most of the capital is the one where the competitive advantage is the least proven.

Do you like what you’re reading so far? If so, consider liking this post or subscribing to support my work!

The Financials

The S-1 filing on May 20th was the first time anyone outside SpaceX got a real look at the books. Here’s what the consolidated picture looks like.

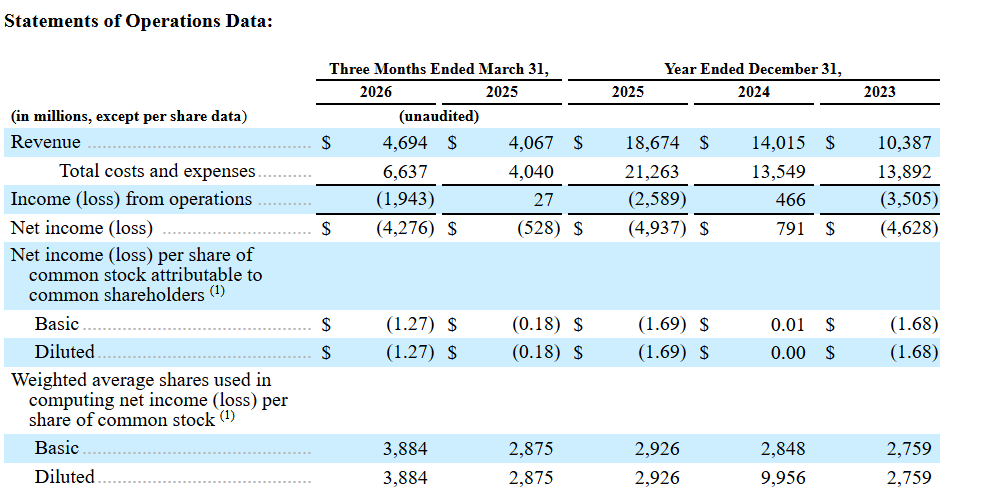

Revenue and losses

$18.67 billion in total 2025 revenue, up 33% from 2024. However, SpaceX swung from a $791 million profit in 2024 to a $4.94 billion net loss in 2025 in a single year. Operating loss was $2.59 billion. Q1 2026 accelerated the pain, with a loss close to $4.3 billion in a single quarter. The trend is moving in the wrong direction on the bottom line. But remember, the Google and Anthropic deals can help in the next few quarters.

The EBITDA number of $6.6 billion is what bulls point to. But EBITDA strips out depreciation on billions of dollars of satellites and rockets that are physically wearing out and need to be replaced. For a company whose core assets are literally flying through space and re-entering the atmosphere at thousands of miles per hour, depreciation is a very real expense.

It’s like saying “If we took away most of our expenses, we’d be profitable.”

The capex problem

Total 2025 capex was $20.7 billion against $18.7 billion in revenue. SpaceX spent more on capital expenditures than it earned in revenue. $12.7 billion of that capex was in the AI segment alone, more than triple what it spent on Space and Starlink combined.

Eisman put it in context on CNBC a few days ago: capex was 42% of revenue in 2023. By Q1 2026 it was 215% of revenue. The AI buildout is consuming the company’s resources.

The balance sheet

Long-term debt at the end of Q1 2026 was $29.1 billion. The $75 billion IPO raise addresses some of that, but a meaningful chunk of the proceeds are going toward funding the continued buildout.

The Amazon playbook?

The bull case is the AWS playbook. Amazon lost money for years building cloud infrastructure that looked like a capital furnace from the outside. Then the margins kicked in and it became the most profitable division in the company. Bulls argue SpaceX is in the same phase with AI compute: heavy investment now, harvest later.

It’s a reasonable analogy. Whether it holds depends on whether AI infrastructure pricing holds up or commoditizes the way most tech infrastructure eventually does. That’s the question.

The Valuation: What Are You Actually Paying For?

The IPO is priced at $135 per share, implying a company valuation of about $1.75 trillion for a company that lost $4.9 billion last year. Let’s look at what serious independent analysts think it’s actually worth.

Aswath Damodaran says it’s worth ~$98 per share

Aswath Damodaran is a professor at NYU’s Stern School of Business and is widely considered the best valuation analyst alive. He ran a full discounted cash flow model after the prospectus dropped and landed at about $98 per share. His model assumes revenues grow from $18.7 billion today to $420 billion by 2036, a 32% annual growth CAGR for a decade. Operating income reaches $158.5 billion. He uses a cost of capital of 8.37% and a terminal growth rate of 4.56%. That produces an enterprise value of about $1.22 trillion. Add the $75 billion of IPO cash proceeds and equity value comes out to roughly $1.3 trillion, or $98 per share.

Worth noting: those are already optimistic assumptions. He’s not using a bear case. He’s using a bull case with generous market size and market share assumptions, and he still gets to $98.

Also worth noting: Damodaran wrote that before the Google deal came out.

Morningstar: $63 per share valuation base case, $154 “moonshot” bull case.

Morningstar values SpaceX at $780 billion in their base case, or about $63 per share. They use mid-teens revenue growth for Space and Connectivity. Their base case AI assumption is 2.4 gigawatts of compute by 2035.

They built three scenarios and probability-weighted them.

The base case, “Minimum Viable Product,” assumes orbital data centers prove viable but capacity-constrained, with SpaceX capturing about 4% of global AI compute by 2035 and generating $47 billion in annual AI revenue. They put this at 50% probability.

The downside, “No Go,” assumes orbital data centers simply don’t work and SpaceX cuts the project around 2028, similar to how Tesla walked away from building a small-car factory. They put this at 43% probability.

The bull case, “Moonshot,” is the only scenario that gets close to $135. It requires Starship to be reusable 85% of the time and orbital data centers to capture roughly 20% of global AI compute by 2040, generating $225 billion in annual AI revenue. Morningstar puts this at 7% probability and it gets you to $154 per share.

The base case math breaks down to: $6.50 from IPO proceeds, $40 from the core space and Starlink businesses, and $16.50 from the probability-weighted AI scenarios. That adds up to $62.51.

Their bull case gets to $152 per share, which is the only scenario any major analyst has produced that actually justifies the $135 offer price. But it requires SpaceX to successfully deploy orbital data centers and capture 21% of global compute power by 2035. That’s an enormous amount of execution on an unproven technology that SpaceX’s own prospectus describes as potentially not commercially viable. Reuters, April 2026

How Much Growth Is Priced In?

Fortune ran a separate analysis and found that at $1.75 trillion, SpaceX would need $1.1 trillion in revenue by 2035 to justify the price. That would require roughly 50% annual revenue growth for nine consecutive years. No company at this scale has ever done that.

So why is it priced at $135?

Because valuation isn’t the only thing that sets IPO prices. Scarcity does. FOMO does. The fact that retail investors have been locked out of SpaceX for 20 years and are now being handed an allocation does. As Investing.com noted, this is partly a scarcity trade. There is no other asset in the world quite like SpaceX and investors are paying up for uniqueness.

That can work as a trade. Tesla has traded at multiples no traditional valuation model can justify for years, and Musk bulls have been right to hold it at times. The risk is that scarcity premiums don’t last forever, and when they unwind, they tend to unwind fast.

The bottom line on valuation

At $135, you’re paying a rich valuation, most likely overpaying. You’re banking on either a sentiment-driven pop you can sell into, or a decade of execution that turns SpaceX into a $1 trillion revenue business. One of those is a trade. The other is a leap of faith.

The Ownership Structure: Musk Has Full Control

SpaceX’s prospectus lays out a two-class share structure. Class A shares, which is what you’re buying in the IPO, carry one vote each. Class B shares carry ten votes each. Musk holds the overwhelming majority of Class B shares, giving him over 85% of total voting power in the company.

A lot of people treat this as a red flag.

I don’t, at least not for the reason most people think.

As a retail investor, I’m a passenger in any large company I own. No individual shareholder is going to meaningfully influence SpaceX’s direction regardless of the governance structure. That’s just the reality of buying into a $1.75 trillion company. The dual-class structure formalizes what’s already true in practice.

More importantly, when I invest in a company, I’m betting on management. And Musk has one of the best track records in business history. He built Tesla from near-bankruptcy into a trillion-dollar company. He built SpaceX into the dominant force in global launch from scratch.

The concerns about his political noise and distraction are real, but the track record speaks for itself. I’d rather have a proven capital allocator with massive personal skin in the game running the show than a committee of professional managers optimizing for quarterly earnings.

Will SpaceX Merge With Tesla?

The one ownership risk worth to consider is that it’s very possible that SpaceX can buy Tesla and create on big company called X. Steve Eisman doesn’t doubt it, for example.

This is where the no-vote structure actually matters. If that merger happens, SpaceX shareholders get loaded up with Tesla’s capital-intensive, highly competitive EV business, and they have zero say in the decision. Eisman’s view is that Tesla’s EV business is being undercut by cheaper Chinese manufacturers and is not a business you’d want to own if you had the choice. SpaceX shareholders wouldn’t have that choice.

This isn’t purely speculative either. Tesla already owns roughly 18.99 million SpaceX Class A shares, converted from its $2 billion xAI investment. The two companies share board members and employees. The groundwork is already laid. It may never happen, but it’s the kind of risk you can’t model and can’t vote against.

Will SpaceX Stock Pop on Day One?

Before getting into the SpaceX-specific setup, it’s worth knowing what the historical data actually says about IPO pops, because it shapes how you should think about this trade.

The average first-day IPO gain from 1980 through 2020 was 18.4%, measured from the offer price. In 2025, Peter Goldstein on LinkedIn said that number was around 34%, the second-best in over a decade.

But here’s the part that matters most: studies show that more than half of large IPOs have negative returns when measured from the opening trade rather than the offer price. The pop happens between $135 and wherever the stock opens. If you’re buying in the aftermarket, you’re not getting that pop. You’re buying into it. The offer price is everything.

Now, for SpaceX specifically. As of two days ago, Reuters said that demand is approaching 4x oversubscribed. That’s a very different picture from the 2x figure circulating earlier this week and it’s a much more encouraging sign for day-one trading. At 4x, you have roughly $225 billion of excess demand chasing $75 billion worth of shares. That kind of imbalance historically creates a big opening pop.

SpaceX is allocating up to 30% of the 555 million shares to retail investors. That’s unusual for a huge IPO, and it can create lots of demand on day one.

The brand recognition is there as well. SpaceX has been a household name for years, and retail investors have been locked out the entire time. That pent-up demand combined with 4x oversubscription is a decent setup for opening day momentum.

The headwinds haven’t disappeared though. Reddit threads still skew skeptical, there’s active anti-Musk sentiment in parts of retail communities, and OpenAI filed its IPO confidentially just one week after Anthropic. Capital will rotate toward the next big offering quickly if SpaceX disappoints.

The most important rule still applies: if it doesn’t pop on day one, the odds it pops in the days after are extremely slim. IPO momentum is front-loaded. If the stock opens flat or breaks below $135, get out and preserve capital even if it means violating the anti-flip period. Missing the next IPO is a much smaller problem than sitting in a broken trade. I can’t stress this enough!

(Unless you get allocated a very tiny position that doesn’t matter).

The Lockup Structure: What Happens After Day One

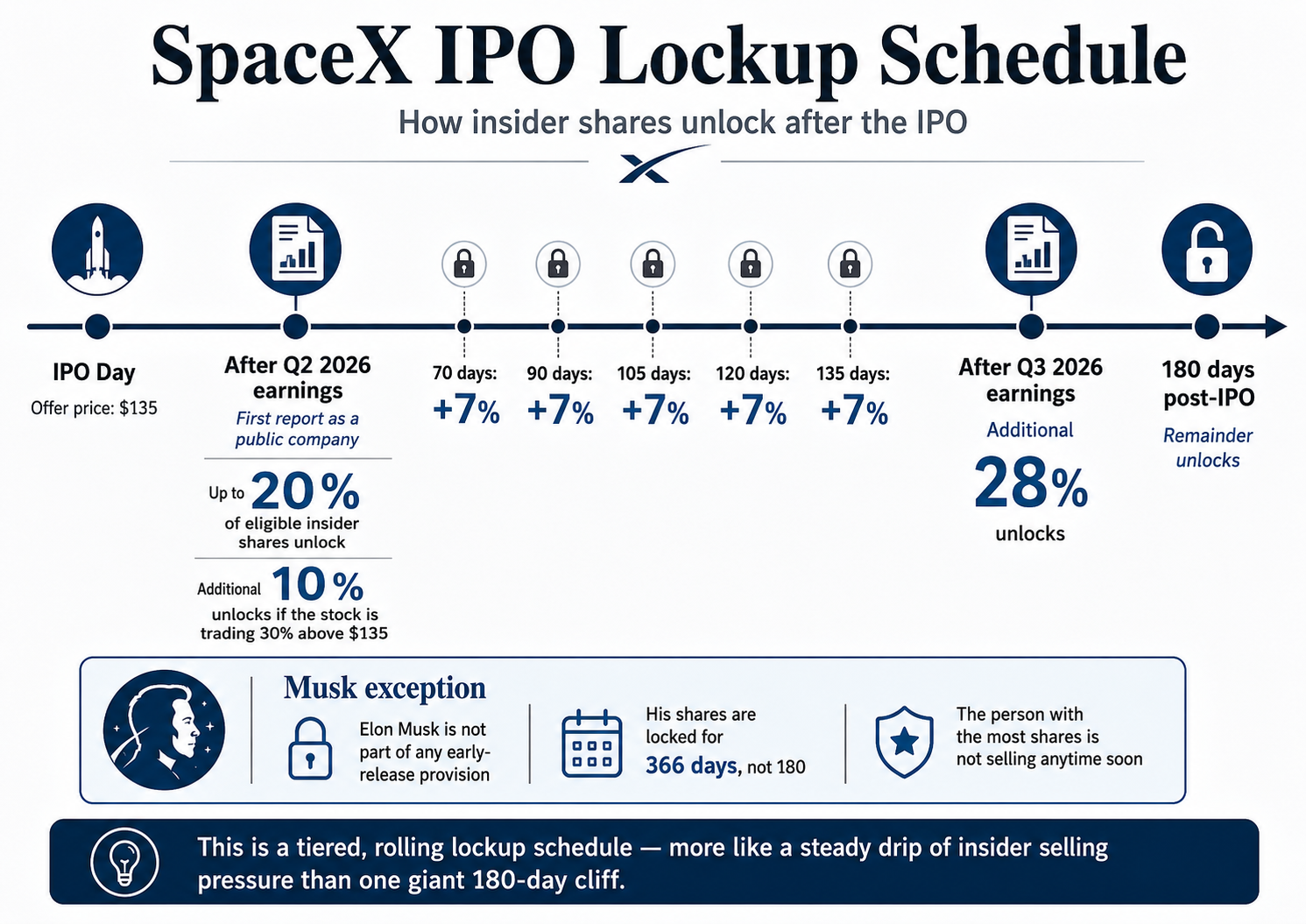

Most IPOs have a simple 180-day lockup: insiders can’t sell for six months and then everything unlocks at once, which typically creates a wall of selling pressure that crushes the stock. SpaceX did something different. Instead of one giant unlock, they built a tiered, rolling release schedule designed to meter selling rather than block it entirely.

Here’s how it works. After Q2 2026 earnings — SpaceX’s first report as a public company — insiders can sell up to 20% of their eligible shares, with an additional 10% unlocked if the stock is trading 30% above $135 at that point. Then, there are five time-based tranches that each release another 7% of shares at 70, 90, 105, 120, and 135 days post-IPO. Another 28% unlocks after Q3 earnings. The remainder unlocks at 180 days.

Musk himself is not part of any early-release provision. His shares are locked for 366 days, not 180. So, the person with the most shares and the most information about the business isn’t selling anytime soon.

Here’s what it means: instead of one cliff in December where billions of dollars of insider shares flood the market, you get a slow, steady drip. That’s better for post-IPO price stability than a standard lockup, but it also means there’s consistent selling pressure from early investors who have been holding for years and are sitting on massive gains.

Are You Allowed To Flip Shares?

The anti-flip rule varies by broker and it's worth knowing yours before you do anything. Among the five U.S. brokers named in the SpaceX prospectus: Fidelity enforces 15 calendar days with escalating penalties up to a lifetime ban on a third offense; Robinhood and SoFi require 30 days, though SoFi's penalties are significantly harsher; and E*Trade also holds to 30 days but is vague on consequences.

I'm trying to get shares through RBC Direct Investing, a Canadian broker. As far as I know, RBC hasn’t published a specific anti-flip holding period for this offering. I could be wrong, but I’ll find out.

The Risks

Government Contract Concentration

About one-fifth of SpaceX’s 2025 revenue came from U.S. federal agencies, mostly NASA, the DoD, Space Force, and the NRO. That’s roughly $3.7 billion a year that exists entirely at the pleasure of government contract renewals.

Musk’s relationship with the Trump administration has been good for business. SpaceX picked up $6.45 billion in new Space Force contracts just weeks before the IPO. But that same political alignment cuts both ways. A new administration, a budget fight, or a falling out could put a meaningful chunk of revenue at risk fast.

Regulatory and China Risk

The direct-to-cell story, Starlink beaming internet straight to your phone without a dish, is one of the biggest subscriber growth narratives in the bull case. But Starlink Mobile still needs FCC approval and foreign regulatory sign-off in every market it wants to enter. The FCC approved 15,000 Gen2 satellites but deferred authorization on the remaining 14,988 SpaceX requested over orbital debris concerns, and won’t sign off on higher power limits for voice and video until further review.

Outside the U.S. it gets messier. Namibia denied Starlink a telecom license a few months ago. Ontario cancelled a $100 million Starlink contract last year over U.S. tariffs. Musk’s public statements are actively making licensing harder in South Africa and other markets. And the S-1 doesn’t even list China as a market while mentioning it as a competitive threat. That’s 1.4 billion people SpaceX almost certainly can never reach. The TAM the prospectus implies assumes global reach that isn’t close to guaranteed.

The AI Contracts Aren’t Locked In

The Anthropic and Google deals together represent close to $2 billion per month at full run rate. But as I said earlier, both have termination clauses that let either party walk after December 31, 2026 with 90 days notice.

Heavy Capex

Capex was 42% of revenue in 2023. By Q1 2026 it was 215%. The AI buildout is eating capital faster than the business generates it. If the orbital data center vision doesn’t pan out, SpaceX will have burned through tens of billions building assets that never deliver the returns the bull case assumes.

Musk Concentration Risk

Musk has a good track record, but the risk is that everything runs through one person. SpaceX, Starlink, xAI, X, Tesla, and Neuralink all depend on him.

My Take and What I’m Doing

SpaceX is a generational business. It has a moat in Space and Starlink, plus Starlink is growing fast, and if the orbital AI thesis actually works, this could look cheap at $135 in ten years.

But I’m not buying it as a long-term hold right now. At $135, you’re paying a price that assumes everything goes right across three very different businesses, one of which has never turned a profit and one of which depends on technology that won’t even be tested until 2028. Damodaran gets to a $98/share valuation. Morningstar gets to $63 base case and only $154 in a big moonshot scenario.

So I’m playing this as a momentum trade. If I get allocated shares through RBC, the plan is simple: if it pops on day one, I’m selling into the strength, most likely. The 4x oversubscription, the retail allocation, the pent-up demand from investors locked out for 20 years, that’s a decent setup for an opening pop and I want to be on the right side of it.

If it opens flat or breaks below $135, I’m out, and I’d possibly consider shorting it depending on the chart because IPOs that flop on day one can just unwind. IPO momentum is front-loaded, and a broken IPO rarely recovers fast. Missing the next trade hurts a lot less than sitting in a losing position with six months of lockup selling pressure dripping overhead.

If you’re thinking about flipping SPCX stock, know your broker’s anti-flip rules before you do anything.

That’s the analysis! Thanks for reading. If you like deep dives like this and weekly watchlists, please consider subscribing. And upgrading to paid will make sure you get full access to all past and future deep dives and watchlists, as well as priority Q&A access.

Disclosure

I’m looking to get shares of SPCX. This article is for informational and educational purposes only and does not constitute financial advice. I'm not a licensed financial advisor. Everything written here reflects my own research and opinions, not a recommendation to buy or sell any security. Do your own due diligence before making any investment decisions. Past performance is not indicative of future results.