Michael Burry Bought MercadoLibre. Should You Buy The Dip?

MercadoLibre’s margins look ugly on the surface. Underneath, the company is still growing like a startup and investing like a long-term winner.

Michael Burry just bought MercadoLibre (MELI) stock in the $1,600s.

He sees value here. That’s despite the company’s falling margins.

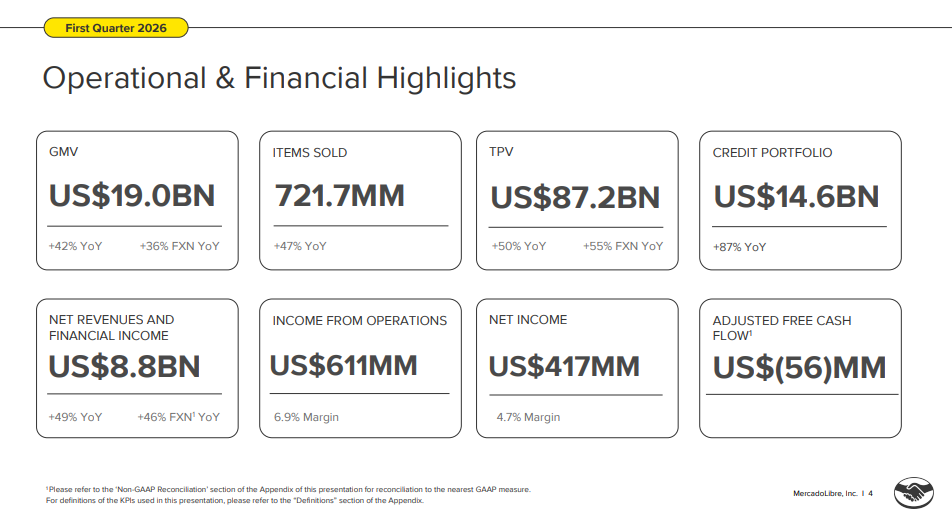

MELI stock fell nearly 13% after reporting solid Q1 earnings.

And if you just looked at the EPS number, you’d understand why. Earnings per share came in at $8.23, down from $9.74 a year ago. That’s a 15.5% decline year-over-year. On the surface, that looks bad.

But here’s the thing. Revenue grew 49% in the same quarter (46% on an FX-neutral basis). That’s the fastest growth pace in almost four years. Total payment volume hit $87.2 billion, up 50%, or 55% fx-neutral. Items sold jumped 47%. Fintech monthly active users reached 82.9 million, up 29% in a single year. That’s roughly the equivalent of adding the entire population of Chile to your platform in 12 months.

So what’s going on? And more importantly, does any of this change the thesis I laid out last month? Let me walk you through it, and if you haven’t checked out my MercadoLibre deep dive from last month, now’s a good time.

Here’s the link:

https://investorscompass.substack.com/p/mercadolibre-deep-dive-the-company

What The Market Reacted To

The EPS miss was the headline ($8.23 in EPS vs. $8.50 expected), but what really scared people was margin compression. Operating income fell 20% year-over-year to $611 million. Operating margin came in at 6.9%, down 600 basis points from a year ago. Gross margin compressed by 3 points.

For anyone who didn’t read the original deep dive, this looks like a business deteriorating. But for those who did read it, this is exactly what I said was coming. Management is spending aggressively on four things right now: free shipping in Brazil, credit card expansion, first-party inventory, and cross-border trade. Every one of those investments pressures near-term margins. None of them are accidents.

The market looked at the EPS line and sold.

The Free Shipping Bet Is Working

Back in 2025, MercadoLibre lowered the threshold for free shipping in Brazil. At the time, investors weren’t thrilled. The concern was that they were giving away margin without a clear payoff.

Q1 2026 makes the payoff very clear.

Brazil GMV grew 38% year-over-year on an FX-neutral basis. Items sold in Brazil grew 56% year-over-year, accelerating from 45% in Q4, 42% in Q3, and 26% in Q2 last year. Volume growth doubled from a high base in just nine months. Unique buyer growth hit 32% year-over-year, which management said was the fastest pace in five years.

And this doesn’t look like low-quality growth either. Conversion improved. Retention improved. Daily active users are growing faster than monthly active users. That means customers aren’t just showing up once because shipping got cheaper. They’re using the platform more often, buying across more categories, and becoming more attached to the ecosystem. That’s exactly what MELI wanted from this investment.

The unit economics are also moving in the right direction. Unit shipping costs in Brazil fell 17% year-over-year in local currency, improving from the 11% decline in Q4. The network is getting bigger and cheaper at the same time.

Quick Thesis Check

In April, I argued that MercadoLibre’s moat is built on multiple layers: a two-sided marketplace network effect, a physical logistics network that took decades to build, and a fintech ecosystem that tens of millions of people now use as their primary financial account.

I also argued that the margin compression was deliberate, temporary, and consistent with a playbook management has run before. Gross margins bottomed in 2020-2021 during the logistics buildout, then recovered to the high 40s by 2022-2023. The current cycle follows the same logic at a larger scale.

One quarter of data doesn’t make or break a thesis. But Q1 2026 moved the needle in the right direction on almost every metric worth watching.

Now let’s get into the parts that actually require some digging.

The rest of this article is for paid subscribers on my Substack. In the full article, I cover some concerns from Q1, the AI developments that actually strengthen the thesis, the updated valuation after the stock dropped, what I’m watching in Q2, and my verdict on the stock.

Paid subscribers also get every past and future deep dive, earnings updates, and the weekly watchlists. If you’ve been on the fence, this is a good time to upgrade!