Microsoft Insider Just Bought $2M Worth. Should You Follow?

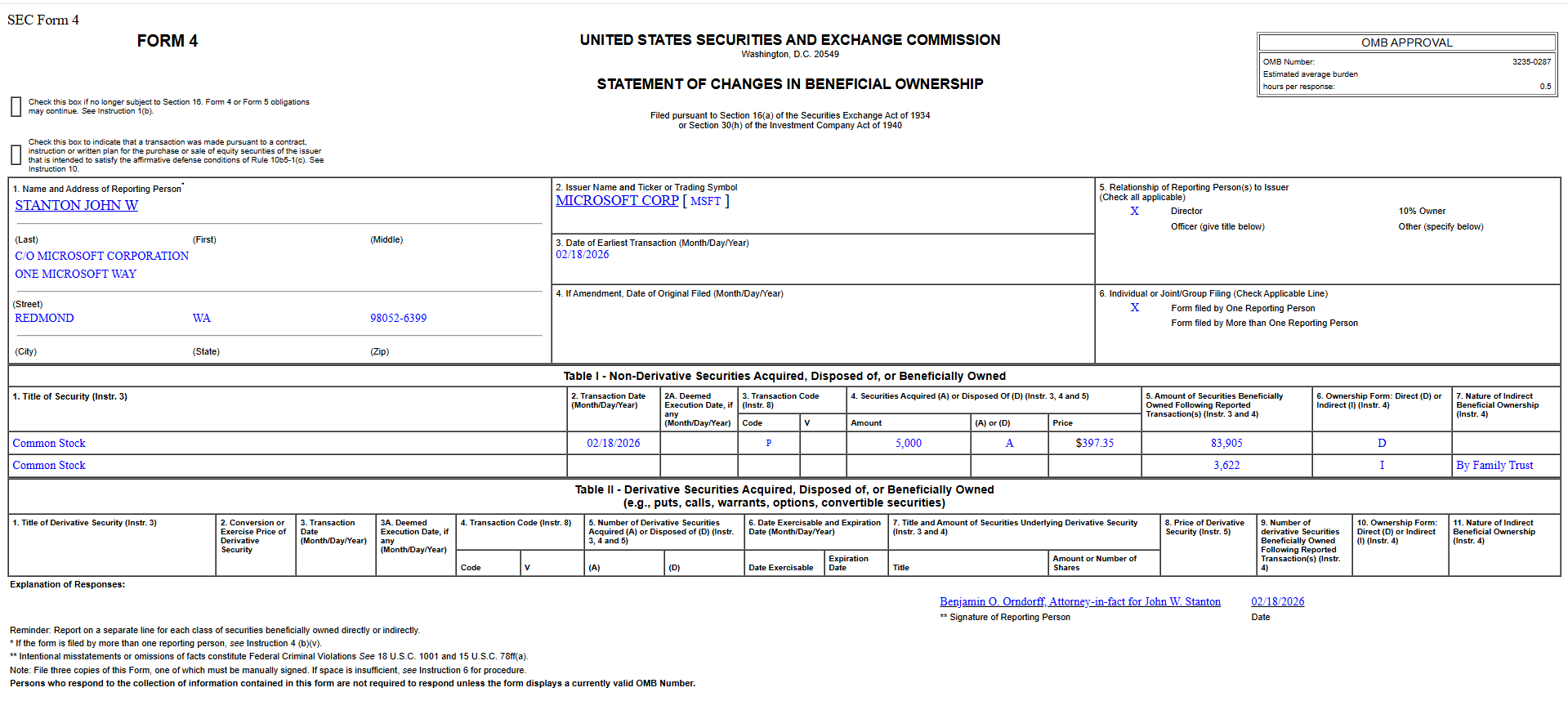

Microsoft insider John W. Stanton (independent director since July 2014) bought $2 million worth of MSFT stock. Should you buy too? The shares were bought for about $397.35 each, and the stock is still around that level now. Let’s dive in.

The First Insider Purchase In A While

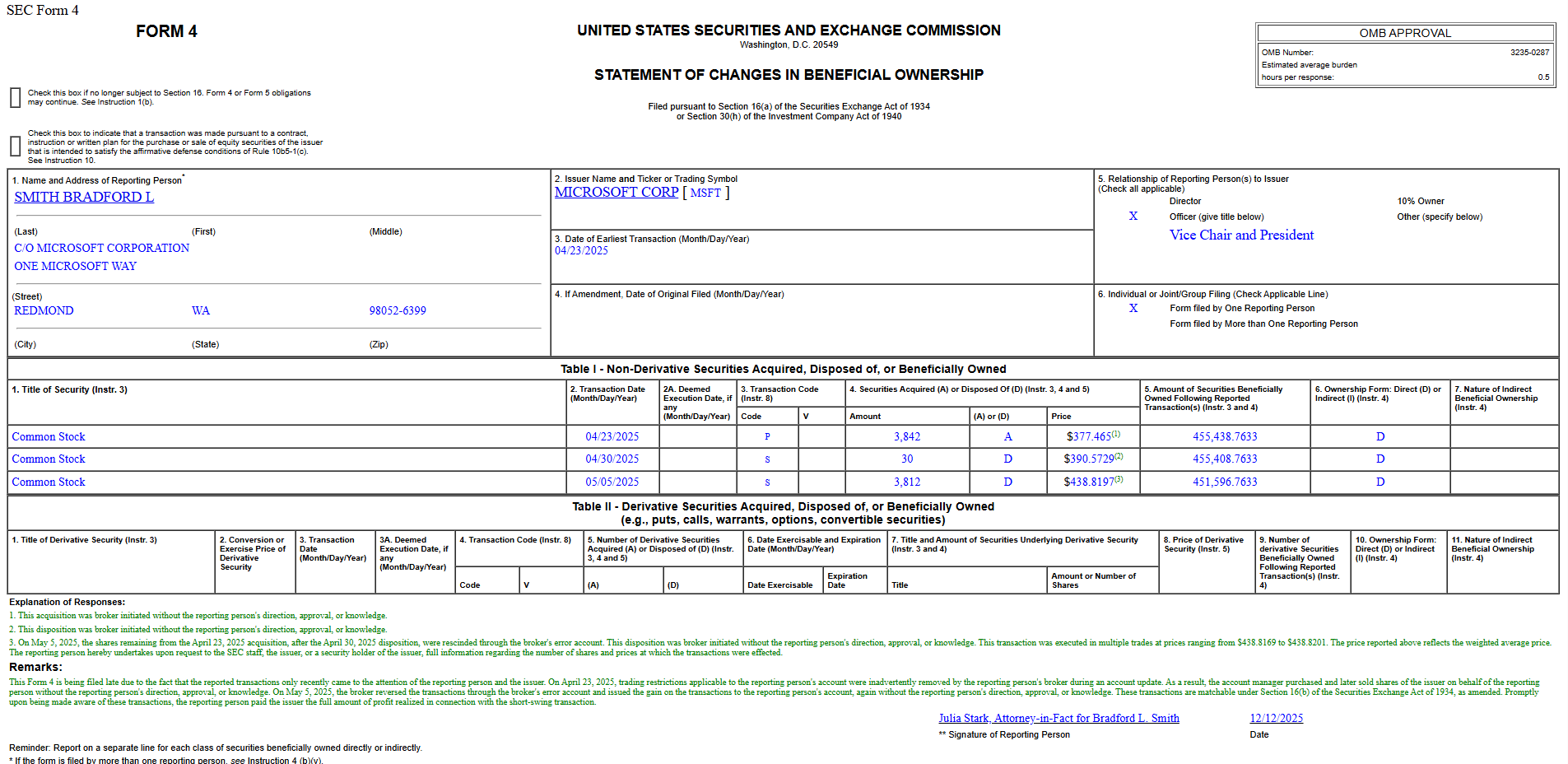

This is actually the first meaningful insider purchase in quite a while. You may see data showing a buy from April 23, 2025 by Microsoft president Bradford L. Smith for about $1.5 million, but that transaction is misunderstood. It shows up in many data feeds as a bullish insider buy, but it wasn’t deliberate investment decision at all. It was actually a mistake. The key details are buried in the fine print of the filing, specifically the little green text in the image below.

If you read the green text at the bottom of that filing, it explains that Smith didn’t choose to buy the shares. His broker accidentally removed trading restrictions on his account, bought stock without his knowledge, and later sold it.

Once the mistake was discovered, the transactions were reversed and he returned the profits. So while it technically shows up as a buy, it wasn’t him deciding the stock was cheap.

This wasn’t a “real” insider buy at all. Stanton’s was, and insider buys on MSFT haven’t been common.

Why Stanton’s Insider Buy Is Different

Stanton’s purchase is different. The filing shows a “P” transaction code, which means an open-market buy. In simple terms, he went into the market and bought shares with his own money at the current price. There’s no note saying it was automatic, compensation-related, or corrected later. He also already owned a large number of shares, and now owns even more both directly and through a family trust.

What Stanton’s Buy Tells Us

The insider buy doesn’t automatically mean Microsoft stock is about to surge, but you know the saying. Insiders can sell for many reasons (tax planning, profit-taking, etc.), but they’ll only buy for one reason — if they think the stock will rise.

This insider buy tells you that someone on the board, with full access to internal information and long-term plans, is comfortable putting real money into the stock at today’s valuation. That puts a dent in the “Microsoft is spending too much on AI CapEx” fears.

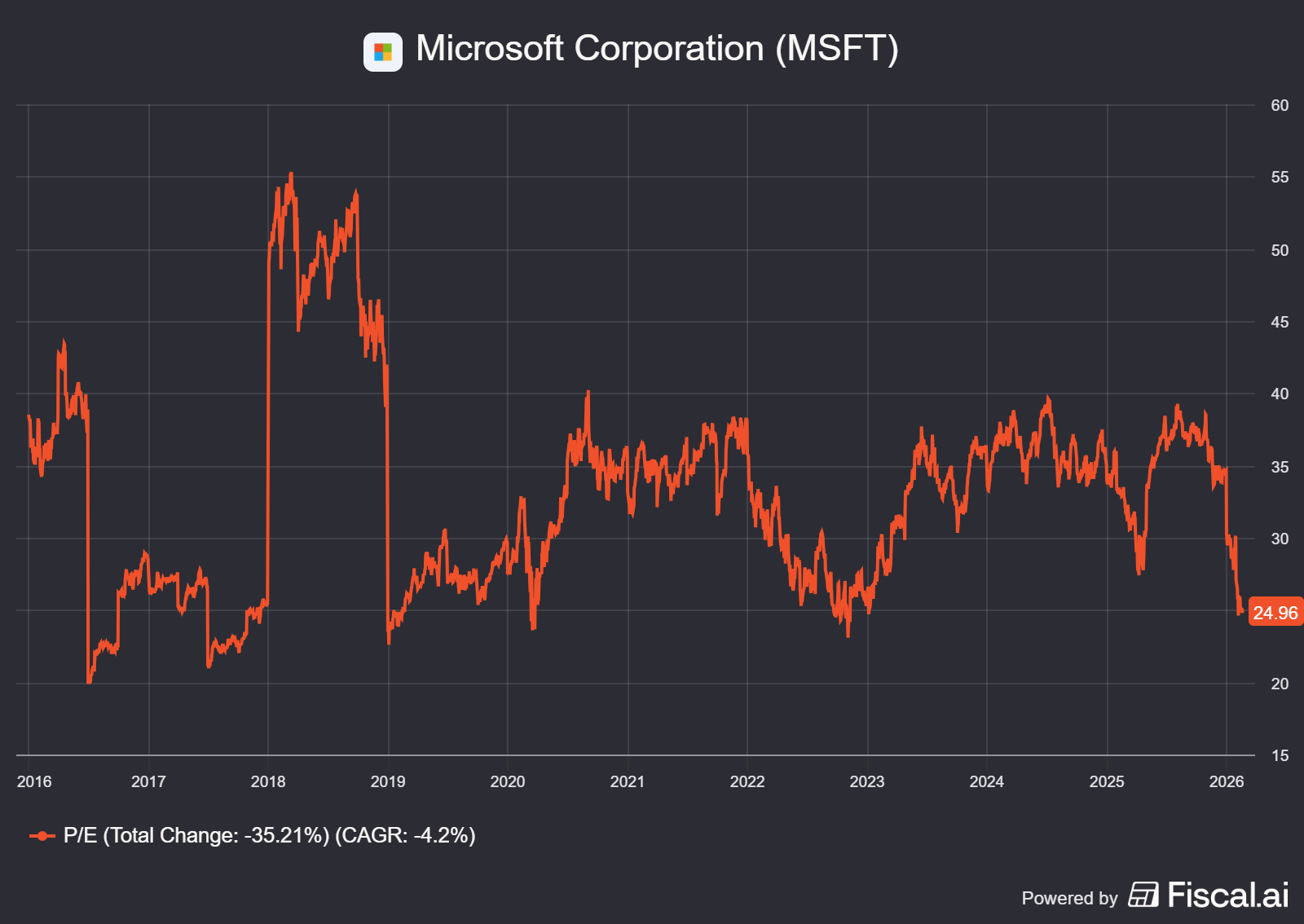

And guess what? His buy lines up with Microsoft’s P/E ratio being relatively low.

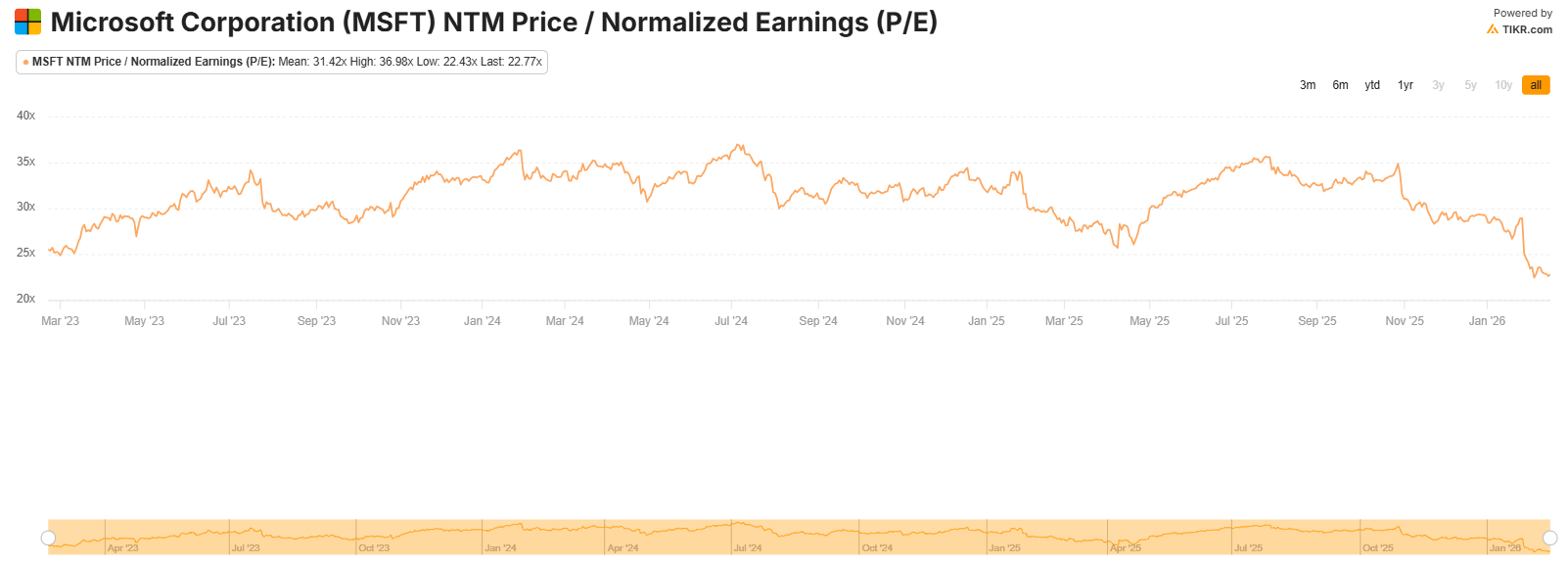

The same can be said about its forward P/E of 22.8x being relatively low compared to its three-year history. Maybe, just maybe, Microsoft’s valuation is good now.

The Chart Is At A Support Too

As I stated in my weekly watchlist:

Chart-wise, it looks like an interesting place to start a position. There’s clear trendline support. If that breaks, the next support is the 200-week moving average (the red line).

Microsoft hasn’t really been under that 200-week moving average since 2011, so a break here would be rare, reinforcing the buy-the-dip thesis. There’s no confirmation of a bounce though so I wouldn’t bet the farm on it.

You can see that in the chart below.

The OpenAI Funding Round Is A Bigger Deal For Microsoft Than It Looks

Now here’s where today’s insider buy connects to something that actually matters for Microsoft’s fundamentals. Bloomberg reported that OpenAI is close to completing the first phase of a new funding round that could top $100 billion, with an overall valuation that could exceed $850 billion. Microsoft is reportedly one of the strategic investors involved in that first phase, alongside names like Amazon, SoftBank, and NVIDIA.

Why is this important? Because one of the main bear arguments in Microsoft’s last earnings call was the size of the OpenAI exposure in its backlog. Microsoft said commercial RPO hit $625 billion, and that roughly 45% of it is tied to OpenAI.

Investors look at that and think, “Okay… but can OpenAI actually pay for all that compute over time?”

A gigantic funding round is basically the cleanest answer to that question. If OpenAI is raising that kind of money, it lowers the risk that they suddenly slam the brakes on spending, renegotiate contracts, or turn into a credit-quality problem. In other words, it makes that OpenAI-driven RPO look more “real” and more collectible, which is exactly what the market has been nervous about.

In even simpler terms, Microsoft’s biggest AI customer just secured the money needed to keep spending aggressively.

It doesn’t mean Microsoft instantly gets new revenue tomorrow, and it doesn’t eliminate every risk either. The same report suggests OpenAI could expand its use of Amazon’s chips and cloud as relationships deepen, which is a reminder that Big Tech partners are also competitors. But zooming out, the big picture is still bullish for Microsoft: OpenAI getting massively funded supports continued AI buildout, continued compute demand, and continued consumption of those multiyear commitments sitting inside Microsoft’s backlog.

It can help Microsoft in another way too: the rising valuation of OpenAI increases the value of Microsoft’s existing 27% stake in the company.

Microsoft accounts for that investment under the equity method, meaning changes in OpenAI’s net assets can flow through Microsoft’s financials. In fact, Microsoft already recorded a large gain tied to OpenAI’s recapitalization in the recent quarter. So if OpenAI’s valuation keeps climbing into the hundreds of billions, that strengthens the paper value of Microsoft’s stake and reinforces the narrative that its early partnership secured a position in one of the most important AI companies in the world.

It’s not cash in the bank unless something is sold, but it still matters for perceived asset value, balance-sheet strength, and investor confidence that Microsoft didn’t just spend heavily on AI. It also owns a piece of the ecosystem it helped scale.

Putting It All Together: Is MSFT A Buy?

When you step back and look at everything in one place, Microsoft has three major things lining up for it: a reasonable valuation, a genuine insider buy, and a support area on the chart. That’s something you don’t see every day with a trillion-dollar company.

On top of that, the biggest fear hanging over the stock — massive AI spending tied to OpenAI — suddenly looks less dangerous with OpenAI nearing a new funding deal. None of these factors alone guarantees upside, but together they create a much stronger setup than any single signal would.

So should you follow the insider buy? Not blindly — insider trades are just one data point, and you should still do your own research.

But this is one of those situations where multiple things line up for a strong company, so I lean bullish. For investors who already believe in Microsoft’s long-term AI dominance and cash-flow engine, this looks less like speculation and more like an opportunity to accumulate a high-quality compounder during a period of doubt.

This article was originally posted on Substack. You can read the original article here.